Embedded finance

This insights page is regularly updated and highlights what Strive Community is learning about embedded finance for small businesses. Do you have best practices or insights to share about this topic? Reach out to us.

Introduction

Embedded finance is a financial product that is placed in a non-financial customer experience, journey, or platform. The digitalization of commerce and business management has led to financial services becoming gradually visible in applications, services, and interfaces that small business owners might use. The promise of embedded finance in serving small businesses lies in its ability to seamlessly integrate into the core business products needed to succeed, such as inventory management and accounting.

As a concept, embedded finance is not new: non-financial service providers have typically offered financial services to customers through non-digital channels, such as retail outlets, supermarkets, and airline agents. Sales financing for household goods (e.g., kitchen appliances) and car loans are other common types of embedded finance. What is new is embedded finance centered around delivering financial services in partnership with technology providers, such as non-financial software platforms, rather than a bank or other traditional financial institution. This allows customers to take advantage of a value-added offering within a familiar digital customer journey. Well-known examples include buy-now pay-later (BNPL) services, such as Zilla (Nigeria) or Splitit (Australia, Japan, UK, US), which allow users to pay for goods and services in regular installments.

For micro- and small businesses that are already digitalized, embedded finance can offer a new channel to access financial services, while encouraging those with limited digital use to improve their digital uptake. Most embedded services for small businesses have a financial core, such as payments, credit, or insurance (see our other insight briefs on these topics). Other categories have started to emerge, such as taxes, accounting, payroll, benefits, and procurement. These can be offered through a range of software, such as e-commerce platforms, gig economy solutions, payments, social media, accounting, financial management, productivity, and collaboration solutions. Many of these platforms are likely to have high levels of small business market penetration and trust and can provide end-to-end solutions for small businesses. For platforms, embedded finance offers a new source of revenue without incurring the costs associated with operating a financial service business.

How embedded finance can address the needs of small businesses

Embedded finance can address micro and small business needs in several ways. Small businesses are likely to have similar financing needs earlier on in their life span. Typical tasks for which a small business might use digital financial services (and therefore embedded finance) include:

- Getting paid for work—for example, selling products and services through a digital platform, such as a marketplace, and receiving payment through the same channel.

- Making payments to suppliers and employees—using a digital service that can receive and make payments, receive and pay invoices, and run payroll.

- Controlling costs—rather than relying on disparate spreadsheets, transaction data can be recorded by the same platform used to send out invoices.

- Managing cash flow—for instance, through accounting software that embeds payments or banking services.

- Managing financial admin—for example, through the same software used to generate invoices and record payments.

- Complying with tax, legal, and regulatory requirements—reminders can be built into apps, for example, through APIs with government agencies, that help small businesses with their reporting requirements.

While there is a limited range of practical insights for organizations supporting small businesses given the relative nascency of embedded finance, this insight brief explores how small businesses can benefit from embedded finance, the demand- and supply-side barriers to adoption and uptake, and the types of embedded financial products that can meet small businesses needs. As a living record of our learning, this insight brief will be updated as we uncover best practices through our partners and program.

The benefits of embedded finance for small businesses

Micro- and small businesses that are already on the path to digitalization stand to benefit significantly, as embedded finance takes advantage of data generated on platforms to better target them with products. These solutions can overcome practical and systemic barriers to finance that small businesses may face in several ways.

1. Platform data underwriting

Digital platform data can enable underwriting via embedded finance, which can benefit small businesses that may lack the traditional data to assess credit risk. Data available through different digital platforms can be used to determine small businesses’ creditworthiness. For example, Khatabook, a business ledger app in India, uses accounts receivable data to assess the creditworthiness of small businesses.

2. Tailored user experiences through collaboration with digital platforms

Digital platforms can offer a better loan application experience than traditional banks. A simple and guided customer experience would allow small businesses to apply for credit in context, reducing the effort required for loan applications elsewhere. For example, Dinie, a pioneer in embedded lending, enables digital platforms to offer business-to-business credit and payment products in Latin America. Dinie also offers overdrafts, risk management, and capital market services. By June 2023, it had disbursed approximately 15,000 loans to 4000 merchants.

3. Offering small businesses customer insights

Companies that offer embedded finance create an anchoring system to educate small businesses about financial services, navigating them to the digital sector in the process. Platforms that embed financial services can also provide additional value-added services, such as financial management and analytics tools. For example, digital platforms have the potential to provide small businesses with customer demographic data that might not otherwise be easily accessible. Merchant marketplaces, such as Shopify, Etsy, and Mercado Libre, can offer small businesses customer engagement information. Similarly, Boost Technology, a Strive Community partner, uses data analysis, behavioral science, and conversational commerce to generate insights for micro and small retailers via WhatsApp to support more informed decisions and drive improved business outcomes.

Embedded financial products for small businesses

Typically, there are five types of embedded digital financial services that small businesses can use.

Embedded lending

Small businesses’ data, such as from sales, order histories, and transaction frequencies, can be used to assess their ability to repay a loan. This data can be a better and more reliable predictor of creditworthiness than other traditional measures, which may not apply to or be appropriate for small businesses. For instance, using real-time sales data rather than historical information, allows modern underwriting models to support embedded lending. This approach enables lenders to bypass traditional, time-consuming data collection processes.

Platforms can pre-qualify borrowers, offer loans when they are most useful, and lend in real time. For example, superapp Grab (a Strive Community partner) enables its merchant and driver partners to access embedded lending products. Similarly, Amazon provides short-term business loans to sellers on the platforms. Sellers are prequalified depending on their transaction history and track record on the platform. In Africa, Jumia Lending offers loans to sellers on the Jumia platform in Nigeria, Kenya, Ivory Coast, and Egypt, in partnership with licensed financial institutions. Sellers with an average weekly sales of $20 or more over the past six months are eligible to receive a loan within 24 to 72 hours.

Embedded payroll

Payroll can be cumbersome for small businesses. Onerous tax regulations and compliance requirements make it challenging to process employees’ salaries on time. Platform-based events, such as clocking in and out, and metadata (such as date, time, and location) can create a payroll file. Payroll solutions on their own can be expensive, but online accounting software that offers this and other functionality would allow small businesses to manage their bookkeeping needs and financial processes. For example, Square, a fintech that has long offered a payment terminal to accept card payments for small businesses, has developed an ecosystem of small business solutions and systems. This includes online payment tools, payroll management, e-commerce site hosting, and customer management tools. Currently, Square is available in eight countries, while its point of sale (POS) systems can accept 130 currencies.

Embedded productive credit and invoice financing

Cash flow is a significant challenge for small businesses, particularly as many operate on thin margins. When stock is low (for instance, for e-commerce retailers), embedded productive credit allows purchase orders to be raised automatically, and supplier payments can be scheduled automatically when orders are received. This can save small businesses time and maintain supplier relations. For example, in Kenya, Uganda, and Ghana, Pezesha works with partner companies, such as Twiga and MarketForce, that integrate its credit-scoring APIs into their platforms to allow their customers to access credit offers in real time. Pezesha works with over 20 partner companies and has extended loans to more than 100,000 businesses.

Invoice financing, also known as accounts receivable financing, allows a small business to borrow against its unpaid customer invoices, improving its cash flow and enabling them to pay short-term expenses. Overdue customer invoices can be a common pain point for many small businesses, who would benefit from accessing invoice financing through existing platforms they use. Through existing data that platforms might have collected on these businesses, with their consent, small businesses can apply for invoice financing and receive funds quickly—sometimes within 24 hours. An example of this is Netherlands-based Rabobank’s partnership with Bizcuit, a digital solution that enables software providers to connect their apps to banks. Small businesses that use Bizcuit to receive payments can use the service to apply for financing.

Embedded insurance

Small businesses can use embedded finance to offer insurance products to their customers, such as insurance to cover e-commerce orders, enabling customers to claim reimbursement if their goods arrive damaged or are lost. Platforms can include pre-negotiated insurance plans to complement products that small businesses buy and sell. For example, Lami, an insurtech in Kenya, allows businesses, such as banks, startups, and other organizations, to partner with them to offer digital insurance products to their users. The product can also be used by these partners to manage their own insurance needs. ARTH offers micro-entrepreneurs in India—particularly women-led small businesses—access to embedded insurance and other payment services.

Embedded incoming payments

As embedded finance continues to evolve, small businesses will be able to set up banking and payment accounts and receive associated payments through platforms. The small business will not have to interact with the underlying banking provider, except perhaps regarding a dispute. For example, Strive Community partner ChatGenie, an e-commerce platform in the Philippines, enables small service businesses to sell inside apps such as Facebook Messenger, Instagram, Viber, GCash, and TikTok. Small businesses can accept bookings and online payments and organize deliveries through these apps—allowing customers to use familiar platforms for regular goods and services.

The untapped opportunity

Embedded payments and banking have tended to be the first products to emerge for small businesses, mainly because they are obvious choices with a broad scope, though embedded insurance services have begun to emerge too. However, providers often focus on payments, cost savings, and cash flow. It is possible that many platforms already offering or looking to offer embedded finance could be missing out on additional opportunities that address the needs of small businesses identified above.

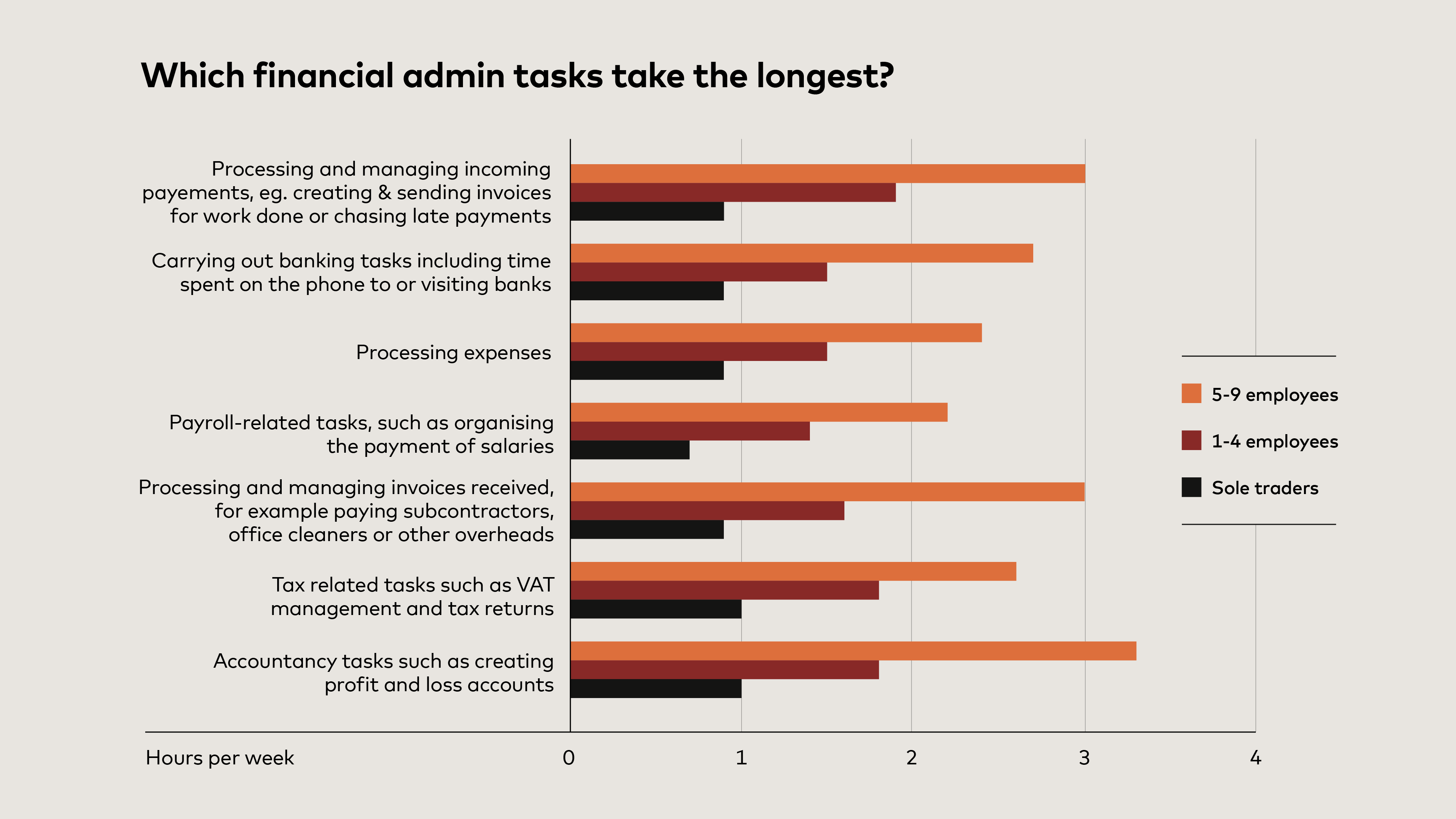

Further, many micro- and small businesses can spend up to four months of the year on financial administration tasks (See below figure). Coupled with the challenge of getting it right, many small businesses may not want to deal with the financial administration and compliance involved in running their businesses. Independent contractors, gig workers, or other small business owners might not know what to do or how to do it. This presents a largely untapped opportunity for digital platforms to use embedded finance to serve their customers—and develop an additional revenue stream in the process.

Figure source: Make Business Simple Report 2020: Starling Bank

Barriers to embedded finance use and uptake by small businesses

While enthusiasm for and interest in embedded financial services has been growing, several high-level factors may be limiting uptake by small businesses.

On the demand side, the adoption of embedded finance by small businesses is likely to be dictated by their comfort level with digital solutions, product awareness, and trust in digital financial services, as well as other competing business priorities. When financial products and services are offered by non-financial institutions, many end users may not consider the source to be trustworthy enough.

On the supply side, barriers can be attributed to financial service providers and other embedded financial value chain players, such as technology providers and platforms.

- Banks and other financial service providers may be unaware of the revenue potential that embedded finance represents. Many banks may be slow to upgrade their legacy technology systems, leading to different priorities around which segment to target first. Some banks with a strong retail history may opt for this approach.

- Financial service providers can also be slow to partner with platform providers; while partnerships stand to benefit all parties, financial service providers can be risk-averse in their collaborations—especially with non-financial organizations.

- Some embedded finance players may not target small businesses at all. This could be a strategic choice, for instance, to focus on retail customers. Digital providers and financial service providers may individually or collectively lack data-sharing frameworks and APIs that can support data sharing among parties.

- A lack of cost-effective electronic know-your-customer (KYC) solutions and processes that can be accessed and used by non-bank providers.

- There may not be suitable digital products available to or relevant to small business users.

- Non-financial service providers interested in lending off their own balance sheets may be deterred by the debt capital requirements.

- Embedded finance requires an enabling regulatory environment and appropriate infrastructure to scale to the smallest and poorest businesses.

Digital and financial service providers will need to consider and address the demand side and supply side barriers to better encourage uptake of embedded financial services for small businesses.

Looking ahead

Embedded finance through platforms is still a young and growing part of the fintech space. By 2025, the global market for embedded financial services is expected to be worth more than $120 billion. Embedded finance is quickly becoming an essential tool for small businesses, with the potential to give them faster access to timely and tailored financial products. These platforms have the potential to close the resource gap between small businesses and corporate organizations, help entrepreneurs weather hard times more confidently and invest in growth more opportunistically.

Three key developments could shape the future of digital financial services for small businesses, particularly regarding embedded finance.

- Business management platforms, such as POS, accounting, and customer relationship management, may partner with banking-as-a-service platforms to launch diverse and scalable financial services.

- Some banks may come to accept their role as wholesalers rather than retailers and may use fintechs as a conduit to embed their financial products in other platforms.

- Platforms or software enablers that own the customer relationship will aim to develop a “one-stop-shop” model for their respective industries.

As we learn more through our program and projects about practices and techniques for offering embedded financial services to small businesses, we will continue to share these insights.